Escape from Flatland

When the Spreadsheet's Perfect World Meets Reality's Messy Truth

The Allure of the God's-Eye View

There’s an image we’re sold of the modern executive: bathed in the cool blue glow of a monitor, they survey a global empire through the clean lines of a dashboard. A master spreadsheet unfurls before them, a digital oracle translating the chaos of the marketplace into a legible, predictable, and controllable world.¹ This is the seductive hum of "data-driven management," a promise that every problem has a quantifiable root and every solution can be modeled. It’s a GPS for business, offering the serene confidence of someone who believes they possess a map of reality itself. As the statistician George Box famously quipped, "All models are wrong, but some are useful." The trouble starts when we forget the first part of that sentence.

This God's-eye view is a dangerous illusion. The very instruments that promise total control, the spreadsheet and the abstract dogmas of the business school, can create a fatal chasm between the model and the messy, unforgiving world of operations. This isn't just about suboptimal decisions; it's a blueprint for catastrophe. The quest for a simplified truth often obscures the complex, human truths that actually determine an organization's fate.

This analysis will deconstruct the twin pillars of this flawed ideology:

The Spreadsheet: It's more than a tool. It has become a worldview, a cognitive framework that flattens the vibrant, unpredictable life of a business into a static grid of cells and "what-if" scenarios.² It’s a lens that tricks us into seeing the world in two dimensions.

"MBA Theory": This is the intellectual framework that legitimizes a detached, quantitative approach to management. In its modern form, it has often prized a pseudo-scientific quest for rigor over professional judgment, ethics, and a grounded understanding of how organizations actually work.³

Together, these forces create a powerful delusion. Theory provides the intellectual justification for a detached worldview; the spreadsheet provides the perfect instrument for its execution. We’ll first examine these forces in isolation before pivoting to four case studies: Wells Fargo, Enron, Theranos, and Boeing, where this thinking fueled spectacular and tragic failures. Finally, we'll explore the profound human cost of this management philosophy and propose a more grounded, reality-based alternative.

The Gospel of the Grid

The spreadsheet was a genuine revolution. Computerized versions of paper accounting worksheets like Excel and Google Sheets rapidly took over the business world, replacing legions of ledger books.² With over 750 million users, Excel became the de facto backbone of enterprise data management.⁵ Its power is undeniable: it wrangles vast amounts of data, enabling complex calculations, forecasts, and shiny charts that make us feel like we know what's coming next.⁵

But over time, the spreadsheet morphed from a useful tool into a dominant ideology. Its very structure, the rigid grid, the deterministic logic of a formula, began to shape how managers see their organizations.² A business becomes a machine of inputs and outputs, a complex but ultimately solvable equation. A problem is something to be modeled in a worksheet, where variables are tweaked until the all-important "profit" cell glows green.

This perspective is supercharged by the language of "data-driven management," which promises to replace fallible human intuition with the cold, hard certainty of numbers.¹ But the glossy brochure of a sophisticated data ecosystem, with integrated CRMs, ERPs, and real-time dashboards, is often a far cry from the reality on the ground.⁷ In countless companies, critical processes like financial planning and supply chain management still run on a chaotic archipelago of disconnected Excel files.⁶ This creates a chasm between the promise of data-driven insight and the brittle practice of spreadsheet-driven management.

When spreadsheets become the central nervous system for collaborative, enterprise-level work, their structural flaws become glaring liabilities.

Version Chaos: How are spreadsheets shared? Email. This inevitably spawns a monster of version proliferation, with multiple users saving multiple local copies.⁶ Nobody knows which file is the "single source of truth," completely undermining the quest for accuracy that was the whole point.⁷

Brittleness and Black Boxes: Enterprise-critical spreadsheets often become monstrously complexa tangled web of convoluted formulas and links to other files, all prone to breaking.⁶ A single incorrect cell reference can silently corrupt an entire financial forecast. The arcane formulas that are a hallmark of "power users" become inscrutable black boxes, their logic known only to the original creator, making them impossible for a team to reliably audit or maintain.⁸

Security Nightmares: Standard spreadsheet files have all the security of a screen door on a submarine.⁶ They can be easily copied, emailed, or downloaded to personal devices. Crucially, they offer no audit trail. It’s impossible to know who changed what, when, or why, a compliance and governance disaster waiting to happen.⁶

Silo Creation: By their nature, spreadsheets are islands. They create information silos that resist integration with core enterprise systems.⁶ Data must be manually exported and imported, a process that is both clumsy and a frequent source of error. This fragmentation makes a holistic, real-time view of the organization impossible.

The very design of the spreadsheet promotes a reductionist, linear view of the world, a perspective fundamentally at odds with the interconnected, non-linear nature of a real business.² It encourages managers to think in terms of isolated "point optimizations" rather than systemic interactions.⁸ Real businesses are complex adaptive systems, full of feedback loops and surprising emergent properties that a simple grid cannot hope to represent.¹⁰

Paradoxically, the strongest evidence of the spreadsheet's failure as an enterprise system is the emergence of an entire industry dedicated to "enterprise spreadsheet management."⁶ These expensive software solutions try to bolt on the features spreadsheets lack: version control, security, and audit trails. It's a tacit admission that we're using the wrong tool for the job and are now paying a premium to patch the holes.

The Theory That Ate the Firm

If the spreadsheet is the tool, the modern business school provides the intellectual and moral justification for its worldview. For decades, MBA programs have faced criticism not just for being irrelevant, but for actively propagating a distorted and harmful view of management.³ As the late, great Peter Drucker said, “Management is doing things right; leadership is doing the right things.” Many business schools seem to have forgotten the second half.

According to scholars Warren Bennis and Jim O'Toole, business schools lost their way when they abandoned their mission to educate professionals and instead adopted a flawed "scientific model."³ This model, they argue, is built on the faulty premise that business is a discipline like chemistry. It elevates the supposed rigor of abstract financial and economic analysis above all else. Faculty are rewarded for publishing in academic journals, not for the competence of their graduates. This has created a culture where complex mathematical modeling is prized, even when it has no connection to how business actually works.³ Things that can't be easily measured, judgment, ethics, morality, are simply assumed away. Yet these are precisely the factors that separate good decisions from catastrophic ones.³

This pretense of science has had profound moral consequences. The late Sumantra Ghoshal argued that by spreading "ideologically inspired amoral theories," business schools have actively freed their students from any sense of moral responsibility.⁴ To make business seem "scientific," theorists had to exclude the messy, unpredictable role of human choice. Since morality is inseparable from human intention, ethics were systematically scrubbed from management theory.¹¹

A prime example is agency theory, a cornerstone of corporate governance courses. It posits that managers (agents) can't be trusted to act in the best interests of shareholders (principals) and must be controlled by rigid monitoring and financial incentives.⁴ Ghoshal saw these as toxic, self-fulfilling prophecies. A theory that assumes people are untrustworthy can, over time, make them less trustworthy by eroding professional norms.⁴ Taught for decades to millions of students, these ideas have become the intellectual air managers breathe, legitimizing a narrow, profit-maximizing ethos.

More recent critiques frame mainstream management theory as a kind of "hoax," like the fable of "The Emperor's New Clothes."¹² This view argues that the theory, much like the emperor's invisible robes, creates "fantasies of control" that stifle critical thinking and normalize cynicism.¹² It presents itself as value-neutral science while concealing a deep-seated set of political and moral values.¹³ This allows the virtues of "capitalist market managerialism" to be "told and sold" without any serious debate.¹³

This intellectual framework finds its perfect expression in the spreadsheet. The amoral, quantitative theories of the classroom are made tangible in the grid of cells. The spreadsheet lets managers build the abstract financial models they were taught, to feel rigorous and scientific while remaining completely disconnected from the operational and ethical realities of their organizations. Theory validates the tool, and the tool operationalizes the theory.

This ideal is starkly contradicted by the observational research of Henry Mintzberg, a perennial critic of the business school establishment. He found that the real work of managers is not systematic and reflective, but is instead defined by "brevity, variety, and fragmentation."¹⁴ As he famously put it, “Management is, above all, a practice where art, science, and craft meet.”

Mintzberg also refutes the idea of strategy being cooked up in an ivory tower. He argues that "strategic planning is not strategic thinking" and that rigid, formal processes often kill the creative, intuitive work that real strategy requires.¹⁵ Effective strategy doesn't emerge from a plan; it emerges from the daily details of the business. The best strategists aren't those who detach themselves; they are those who immerse themselves, able to see the strategic signals in the operational noise.¹⁵ This view of management as a hands-on "craft" is the polar opposite of the detached, analytical model promoted by the establishment. The critique is no longer just that business schools are failing to teach useful skills, but that they are actively instilling a harmful ideology, one that is amoral, reductionist, and dangerously detached from reality.⁴

When Models Fail: Four Portraits of Catastrophe

The dangers of this mindset are not theoretical. In the real world, this philosophy has been a central actor in some of the most spectacular corporate disasters of our time. These are not stories of a few "bad apples"; they are systemic failures, predictable outcomes of a management culture that prioritizes the elegance of the model over the complexity of reality.

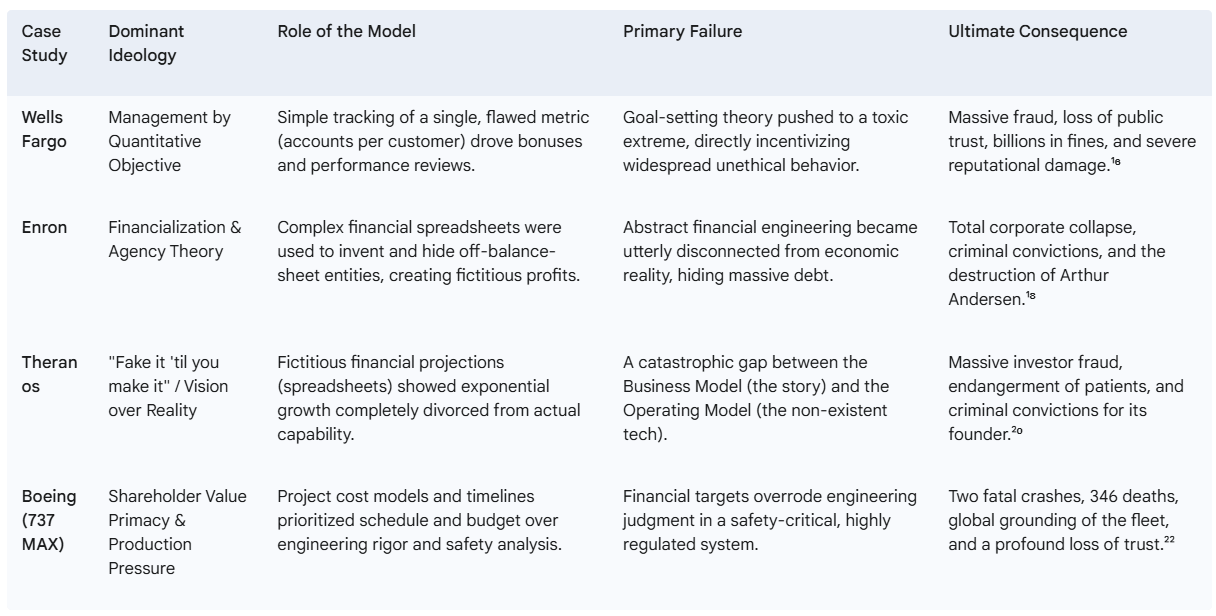

Case Study 1: Wells Fargo, The Tyranny of the Target

At Wells Fargo, the philosophy was brutally simple: sell more stuff. This devolved into the infamous "Eight is Great" strategy, a relentless push for employees to sell eight different financial products to every single customer.¹⁷ This wasn't a suggestion; it was a mandate. Branch managers had daily quotas, and failure meant demotion or termination.¹⁷ Performance was tracked on scorecards, and bonuses were tied directly to hitting the numbers.²⁷ As one former employee told investigators, “You have to meet your goals… If you don’t meet your goals, you’re not a team player.”

This is management by simplistic, quantitative objectives taken to its toxic conclusion. The obsessive focus on one easily measured metric, accounts opened, completely ignored how those goals were being met.²⁸ Faced with impossible targets, thousands of employees did the only thing they could to keep their jobs: they cheated. They opened over 3.5 million unauthorized bank and credit card accounts, often forging signatures or enrolling customers in services without their knowledge.²⁵ The result was a scandal of epic proportions, leading to billions in fines and a catastrophic breach of trust.¹⁶

Case Study 2: Enron, The Alchemy of Abstraction

If Wells Fargo was a failure of simple metrics, Enron was a failure of sophisticated abstraction. Enron’s collapse was rooted in its use of complex financial engineering and an aggressive form of mark-to-market accounting.¹⁹ This allowed the company to hide billions in debt and book projected future profits as current income, creating a dazzling illusion of success.¹⁹ Jeff Skilling, the company’s CEO, once declared, "We are the good guys. We are on the side of angels." Reality disagreed.

Enron was the apotheosis of detached, amoral MBA theory. The company's financial statements weren't a reflection of reality; they were a theoretical construct, built in complex spreadsheets. This created a fatal disconnect from the operational truth of cash flow.¹⁸ While the company reported that its revenue grew 750% between 1996 and 2000, it was hemorrhaging cash.¹⁸ The "innovative" models became a tool for perpetrating one of the largest accounting frauds in history, leading to the company's spectacular collapse.¹⁹

Case Study 3: Theranos, The Business Model Without a Business

The story of Theranos is a stark lesson in the difference between a business model and an operating model.³⁰ The business model, the "what" and "why", was genius. Elizabeth Holmes pitched a revolutionary blood-testing technology that could run hundreds of tests from a single finger-prick of blood.²¹ The narrative was visionary and wildly attractive to investors. As Holmes herself said, "The minute that you have a backup plan, you've admitted that you're not going to succeed." She had no backup plan.

The problem was the operating model, the "how", was non-existent. The technology never worked.²⁰ Product demos were faked, often using secretly modified machines from competitors.²⁰ The company sold investors a story backed by nothing more than fictitious spreadsheet projections. In one instance, Theranos projected $1 billion in revenue for 2015 when its actual revenue in 2014 was around $100,000.²¹ Lured by the powerful narrative, supposedly sophisticated investors poured over $900 million into the company, failing to conduct basic operational due diligence.²⁰ The void where the operational reality should have been was papered over with a really, really convincing spreadsheet.²¹

Case Study 4: Boeing, The Unbearable Pressure of Production

The Boeing 737 MAX tragedy is arguably the most devastating example of what happens when spreadsheet logic collides with the unforgiving physics of a safety-critical industry. Facing intense competition from Airbus, Boeing's management needed a new, more fuel-efficient 737, and they needed it fast and cheap.²²

The engineering solution involved placing larger engines further forward on the wing, which altered the plane’s aerodynamics and made its nose tend to pitch up. To counteract this, engineers developed the Maneuvering Characteristics Augmentation System (MCAS), a piece of software designed to automatically push the nose down.²³

But management decisions, driven by financial models, led to a series of fatal compromises. The power of MCAS was increased during development, but key design documents weren't updated.²² To minimize costs and the need for expensive pilot retraining, the system's existence was downplayed to airlines and regulators. It was designed to rely on a single sensor, creating a single point of failure with catastrophic potential.²³ An investigator on the congressional report would later call MCAS "the monster in the closet."

This is a textbook case of "production pressure," where meeting schedules and budgets is valued more than working safely.²⁴ In a software company, this might lead to a buggy product. In aerospace engineering, it led directly to two crashes and the loss of 346 lives. The optimistic plan, born of financial pressure, failed to adapt to a dynamic and dangerous operational reality.

The Human Cost of Unreality

The consequences of this detached management philosophy are not confined to balance sheets. This approach inflicts a profound and lasting human cost on employees, customers, and society. It creates environments where ethical compromises become a condition of employment and safety is subordinated to production.

The link between unrealistic goals and unethical behavior is direct and well-documented. As argued by Harvard Business School Professor Lynn S. Paine, corporate misconduct is often the result of decent people being placed in untenable situations.³² At Sears Auto Centers, a shift to a commission-based pay structure with demanding quotas led service advisors to systematically lie to customers about needed repairs just to keep their jobs.³²

This pressure creates a toxic, cutthroat culture.³³ Employees are forced into a conflict where their livelihood is pitted against their ethical obligations.²⁶ When faced with the choice between acting ethically and being fired, a predictable number will choose to protect their family.³⁴ This creates a systemic moral hazard. Senior leadership, operating from the comfort of their spreadsheets, sets the aggressive targets. They create the risk. But the consequences fall on frontline employees, who are forced to make the compromises. When the scandal breaks, the first response is often to blame a "small number of our team members" and fire thousands of low-level workers, while senior leadership deflects responsibility.²⁶

In industrial settings, this same pressure is a direct threat to safety. "Production pressure" describes an imbalance where the value of production, meeting schedules and budgets, overwhelms the value placed on safety.²⁴ It’s a slow, gradual degradation of safety margins. Shortcuts become necessary to meet unrealistic deadlines, and these at-risk behaviors become normalized because they are implicitly rewarded for "getting things done."²⁴

Many safety programs rely on lagging indicators, like accident rates.³⁶ These metrics only tell you what happened after things went wrong. A robust safety culture focuses on leading indicators, measuring protocol adherence before it leads to an accident.³⁵ The pressure for production, however, incentivizes ignoring these leading indicators in favor of hitting the numbers.³⁵

The constant strain of meeting unrealistic targets is a major contributor to employee burnout.³⁷ This isn't weakness; it's a state of physical, emotional, and mental exhaustion caused by chronic workplace stress.³⁸ Burnout leads to declining productivity, cynicism, and severe health consequences like anxiety and depression.³⁹ The pressure to perform, born from an abstract model, ultimately destroys the human capacity to do so. It reflects what leadership experts Steve Gruenert and Todd Whitaker observed: "The culture of any organization is shaped by the worst behavior the leader is willing to tolerate."

Escaping the Flatland

The failures of Wells Fargo, Enron, Theranos, and Boeing were not failures of data. They were failures of wisdom. They were the predictable consequence of a management philosophy that substitutes the simplicity of a model for the complexity of reality. The pursuit of a God's-eye view through the two-dimensional flatland of the spreadsheet is a dangerous fantasy.

Escaping this trap requires more than just better tools, though they certainly exist. A host of modern software platforms offer integrated systems that provide a single source of truth and overcome the spreadsheet's limitations.⁴¹ But a new tool isn't enough. A new mindset is required. Two philosophies offer a path toward a more grounded and humane form of management.

The Lean Alternative: Go to the Gemba Lean Management offers a powerful antidote to the detached, top-down approach. Its core principle is a radical shift: from managing by results to managing by process.⁹ The central tenet is to lead from the gemba, the Japanese term for "the actual place" where work happens, not from an office chair.⁹ It demands that managers observe, listen, and learn from the people actually doing the work. Employees are not costs to be minimized, but the organization’s most valuable asset.⁹

The Systems Thinking Alternative: Seeing the Whole Picture Systems Thinking is a direct counterpoint to the reductionist models of the business school. It is a holistic approach focused on understanding the interconnections and feedback loops that make up a complex system.¹⁰ Instead of breaking problems into isolated parts, a systems thinker seeks to understand the whole. This mindset encourages leaders to look for the hidden structures and mental models that give rise to surface-level events.⁴² It helps managers anticipate ripple effects and unintended consequences.¹⁰

The choice facing modern leadership is clear. They can continue to manage the model, optimizing a spreadsheet representation of the business while remaining blind to the accumulating risks and the growing human cost. Or, they can choose to lead the reality. This requires embracing management as a craft, as Henry Mintzberg described it. It requires leaders to be deeply embedded in the details of their operations, to see the whole system in all its complexity, and to respect the people who bring that system to life. As the great systems thinker Donella Meadows said, "We can't control systems or figure them out. But we can dance with them."

References

Provost, F., & Fawcett, T. (2013). Data Science for Business: What You Need to Know about Data Mining and Data-Analytic Thinking. O'Reilly Media.

Levy, S. (1984). "A Spreadsheet Way of Knowledge." Harper's Magazine. This article is a seminal, early critique of how spreadsheet software shapes thinking.

Bennis, W. G., & O'Toole, J. (2005). "How Business Schools Lost Their Way." Harvard Business Review.

Ghoshal, S. (2005). "Bad Management Theories Are Destroying Good Management Practices." Academy of Management Learning & Education.

Harris, S. (2012). "750M Users of Microsoft Excel—Are You One?" Reuters Events. While more recent estimates are higher, this figure aligns with the period when many of the cited critiques began to emerge.

PwC. (2004). "The use of spreadsheets – considerations for Section 404 of the Sarbanes-Oxley Act." This report details many of the common control failures and risks associated with enterprise spreadsheet use.

Olson, D. L. (2004). Managerial Issues of Enterprise Resource Planning Systems. McGraw-Hill/Irwin. Discusses the importance of integrated systems for creating a "single source of truth."

Powell, S. G., & Baker, K. R. (2017). Business Analytics: The Art of Modeling with Spreadsheets. Wiley. While a textbook on how to use spreadsheets, it implicitly highlights the linear, component-based thinking they encourage versus more dynamic modeling.

Liker, J. K. (2004). The Toyota Way: 14 Management Principles from the World's Greatest Manufacturer. McGraw-Hill.

Meadows, D. H. (2008). Thinking in Systems: A Primer. Chelsea Green Publishing.

Ghoshal, S. (2005). "Bad Management Theories Are Destroying Good Management Practices." Academy of Management Learning & Education. The argument on morality and intentionality is a key part of this paper.

Boje, D.M., Luhman, J.T., & Cunliffe, A.L. (2003). "Mainstream management theory: the hoax of the Emperor's new clothes." Journal of Management Inquiry.

Klikauer, T. (2013). Managerialism: A Critique of an Ideology. Palgrave Macmillan.

Mintzberg, H. (1990). "The Manager's Job: Folklore and Fact." Harvard Business Review. (Reprint of his 1975 article).

Mintzberg, H. (1994). The Rise and Fall of Strategic Planning. Free Press.

Consumer Financial Protection Bureau. (2016). "CFPB Fines Wells Fargo $100 Million for Widespread Illegal Practice of Secretly Opening Unauthorized Accounts."

Eisinger, J. (2017). The Chickenshit Club: Why the Justice Department Fails to Prosecute Executives. Simon & Schuster. Provides a detailed account of the "Eight is Great" culture.

McLean, B., & Elkind, P. (2003). The Smartest Guys in the Room: The Amazing Rise and Scandalous Fall of Enron. Portfolio.

Healy, P. M., & Palepu, K. G. (2003). "The Fall of Enron." Journal of Economic Perspectives.

Carreyrou, J. (2018). Bad Blood: Secrets and Lies in a Silicon Valley Startup. Knopf.

U.S. Securities and Exchange Commission. (2018). "SEC v. Elizabeth Holmes, Theranos, Inc., and Ramesh “Sunny” Balwani." Complaint filing.

U.S. House of Representatives Committee on Transportation and Infrastructure. (2020). "The Design, Development & Certification of the Boeing 737 MAX." Final Committee Report.

National Transportation Safety Board. (2019). "NTSB Issues 7 Recommendations to FAA to Improve Safety of Automated Control Systems."

Dekker, S. (2014). The Field Guide to Understanding 'Human Error'. Ashgate.

Tappe, A. (2017). "Wells Fargo finds 1.4 million more unauthorized accounts." CNNMoney.

Corkery, M. (2016). "Wells Fargo’s C.E.O. Is Contrite Before Angry Senators." The New York Times. Coverage of John Stumpf's testimony.

Tolentino, J. (2016). "The Ethical Rot of Wells Fargo’s Business Model." The New Yorker.

Ordóñez, L. D., Schweitzer, M. E., Galinsky, A. D., & Bazerman, M. H. (2009). "Goals Gone Wild: The Systematic Side Effects of Overprescribing Goal Setting." Harvard Business School Working Paper.

McLean, B., & Elkind, P. (2003). The Smartest Guys in the Room.

Feloni, R. (2018). "The fatal mistake that led to the downfall of Theranos." Business Insider. An example of the common post-mortem analysis of its business vs. operating model.

Carreyrou, J. (2018). Bad Blood.

Paine, L. S. (1994). "Managing for Organizational Integrity." Harvard Business Review.

Ordóñez, L. D., et al. (2009). "Goals Gone Wild."

Bazerman, M. H., & Tenbrunsel, A. E. (2011). Blind Spots: Why We Fail to Do What's Right and What to Do about It. Princeton University Press.

Occupational Safety and Health Administration (OSHA). (2016). "Using Leading Indicators to Improve Safety and Health Outcomes."

OSHA FactSheet. "Recording and Reporting Occupational Injuries and Illness." Details lagging indicators like TRIR.

World Health Organization. (2019). "Burn-out an 'occupational phenomenon': International Classification of Diseases."

Maslach, C., & Leiter, M. P. (2016). "Understanding the burnout experience: recent research and its implications for psychiatry." World Psychiatry.

Mayo Clinic Staff. "Job burnout: How to spot it and take action."

Maslach, C., Jackson, S. E., & Leiter, M. P. (1996). Maslach Burnout Inventory Manual. Consulting Psychologists Press. Cynicism/detachment is a core component of the MBI framework.

Gartner, Inc. "Magic Quadrant for Cloud Financial Planning and Analysis Solutions." An example of industry analysis of modern, integrated software that replaces standalone spreadsheets.

Senge, P. M. (1990). The Fifth Discipline: The Art and Practice of the Learning Organization. Doubleday/Currency. The "iceberg model" is a widely used metaphor to explain the concepts in Senge's work.